PepsiCo’s revenue falls, but its stock price continues to rise. What is the secret behind the popularity of PepsiCo shares?

Despite the challenges PepsiCo Inc. (NYSE: PEP) has faced, its stock price has been rising steadily. On 8 October, the company released its Q3 2024 report, posting revenue lower than the corresponding period in 2023. Nonetheless, the stock price continued its upward trajectory.

Based on the quarterly earnings report, this article provides a fundamental analysis of PEP stock, describes its business model, assesses how inflation impacts its revenue and performs technical analysis of PepsiCo stock. From this analysis, a forecast for the stock price at the end of 2024 has been prepared.

About PepsiCo Inc.

PepsiCo Inc. is an American multinational corporation that produces and sells food, soft drinks, and snacks. Its portfolio includes famous brands such as Cheetos, Gatorade, Lay’s, Mountain Dew, Pepsi, Quaker, and Tropicana. The company was founded in 1965 by merging Thе Pepsi Сola Company and Frito-Lay. On 13 November 1972, PepsiCo Inc. went public on the NYSE, and since then, its shares have been traded under the PEP ticker symbol.

PepsiCo Inc.’s business model

PepsiCo divides its operations into three major segments, publishing information on each separately in its quarterly reports. Below are the segments in which the company operates:

- Frito-Lay: here, PepsiCo focuses on producing and selling various snacks. The range includes products from many popular brands (Cheetos, Doritos, Lay’s, Ruffles, and Tostitos). Its leading position in the US salty snack market is supported by these high-margin products

- Quaker Foods: this includes Quaker products, one of the pioneering brands in PepsiCo’s portfolio, which specialises in healthy eating. Quaker offers cereal bars, cereals, muesli, oatmeal, and other products. This sector focuses on breakfast and healthy eating products

- PepsiCo Beverages: this segment represents the entire range of PepsiCo’s drinks, including soft drinks (Mountain Dew, Pepsi), sports and energy drinks (Gatorade), purified drinking water (Aquafina), tea, and juices (Lipton, Tropicana). Drinks are the company’s core business and generate the majority of revenue

In its reports, PepsiCo provides detailed information for each segment only in North America, while revenues from other regions are presented as a consolidated total. PepsiCo’s business model demonstrates that it operates across three markets simultaneously, enabling it to diversify its revenues.

PepsiCo Inc.’s Q3 2024 report

On 8 October, PepsiCo reported its financial results for Q3 2024. Below are the key figures from the report:

- Revenue: 23.32 billion USD (-0.6%)

- Net income: 2.93 billion USD (-5.0%)

- Earnings per share: 2.13 USD (-4.9%)

- Operating profit: 3.87 million USD (-3.6%)

Revenue by segment:

- Frito-Lay North America: 5.89 billion USD (-1.2%)

- PepsiCo Beverages North America: 648.00 million USD (-13.2%)

- Quaker Foods North America: 7.17 billion USD (+0.1%)

Revenue by region:

- Latin America: 2.91 billion USD (-4.6%)

- Europe: 3.94 billion USD (+6.4%)

- Africa, Middle East, and East Asia: 1.55 billion USD (-6.2%)

- Asia-Pacific region: 1.19 billion USD (-1.4%)

PepsiCo’s management noted that the company demonstrates resilience despite challenging conditions. The main issues in Q3 were the recall of Quaker products due to potential Salmonella contamination and geopolitical tensions in some international markets.

CEO Ramon Laguarta emphasised that the company remained profitable thanks to strict cost control and investments in its competitiveness. However, in light of these challenges, PepsiCo has revised its Q4 and full-year 2024 forecast. Revenue growth is now expected to be lower than the previous estimate of 4%, while the forecast for EPS growth remains at least 8%. Therefore, PepsiCo maintains a positive outlook for the full year 2024.

Although financial performance fell short compared to last year’s corresponding period, the company’s stock price rose following the financial release.

How inflation impacts PepsiCo Inc.’s revenue

Experts are increasingly suggesting online that US inflation may begin to rise again and exceed the 2022 figures. If these forecasts materialise, how could this influence the company’s revenue? It is impossible to predict reliably how exactly things will evolve. However, we can analyse past periods when the company operated amid both high and low inflation.

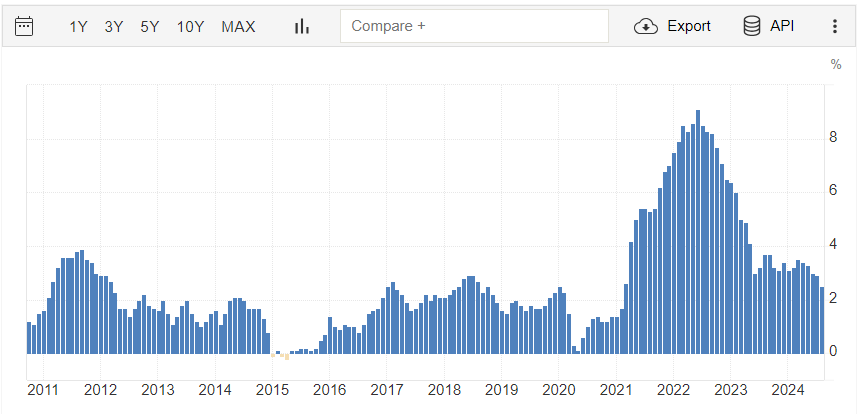

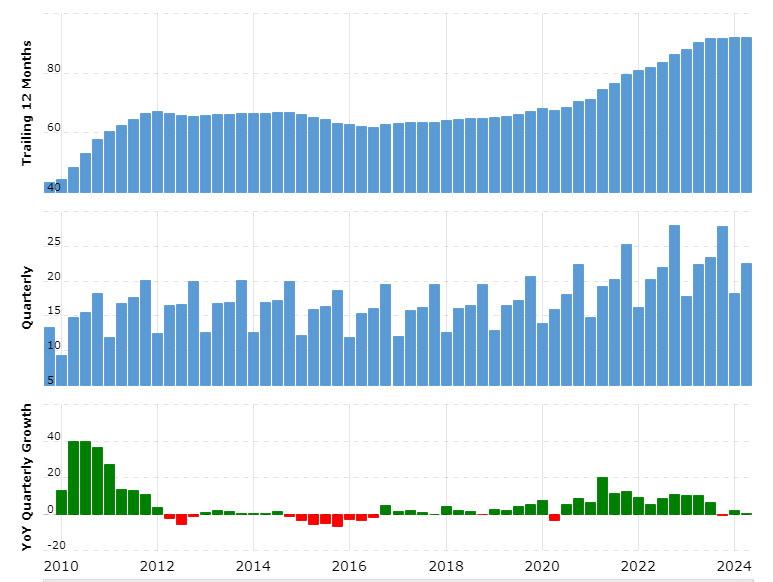

In 2020, the crisis caused by the coronavirus pandemic brought the restaurant business, one of the segments where the company operates, to the brink of survival. US inflation eased to 0.1% in 2020. After the restrictions on visiting public spaces were lifted, the restaurant business began to revive, with inflation heading upwards. By June 2022, the annual inflation rate in the US reached a peak of 9.1%. Surprisingly, the company’s revenue was almost unaffected during this period. It failed to outperform the 2019 figures only in Q2 2020, and by June 2022, the average annual growth in quarterly revenue was about 10%. Below is the data on US inflation and PepsiCo’s revenue over the past 14 years.

The infographics show that the company’s revenue slows or declines when inflation falls to zero. When inflation rises above 2.0%, financial inflows start to surge.

Why does revenue grow when inflation accelerates? With inflation on the rise, costs for commodities, transport, and labour increase. In response, the company raises prices for its products. Thanks to the strong reputation of the brands (Frito-Lay, Pepsi, and Quaker), consumers tend to remain loyal to their preferences despite galloping prices. As a result, an increase in the cost of products, particularly everyday items purchased frequently, drives nominal revenue even if sales drop. This allows the company to maintain its revenue at a high level.

When inflation rises, PepsiCo actively invests in innovation to reduce the impact of inflation on the cost of its products. For example, this may include reducing the packaging size or using cheaper packaging materials. These measures enable the company to control costs, which helps stabilise the operating margin. Afterwards, when inflation begins to fall and the company’s revenue growth slows, the business remains profitable thanks to previous optimisation measures. This approach allows the company to increase dividend payouts to its shareholders, making PepsiCo shares attractive for long-term investments.

As a result, regardless of how the US economic situation evolves, PepsiCo’s business model remains resilient to such challenges. Only a prolonged period of deflation could pose a serious risk to the company.

If we look at PepsiCo stock’s historical performance, it is clear that it is ideal for long-term investors, especially given that the shares have been trading in an uptrend since 1974. A decline in the stock price during crises or challenges the company has faced has always been followed by a subsequent rise.

In July 2021, the shares surpassed the upper line of the ascending channel and headed towards new highs, forming a new ascending channel, where they are trading as of mid-October 2024. Based on this information, two forecasts for PepsiCo shares can be considered for the final part of 2024.

The optimistic forecast for PepsiCo stock in 2024 suggests further stock price growth within the ascending channel to the 188 USD resistance level. A breakout of this level will drive the price to the channel line between 200 and 210 USD. The slower the quotes move upwards, the higher the channel boundary.

The pessimistic forecast for PepsiCo stock for 2024 suggests a correction, as part of which the quotes may break below the 160 USD support level. If this occurs, the stock price could fall to 140 USD, where the correction will likely end, and the quotes will head upwards again.

Summary

The Q3 2024 report did not reveal significant problems at PepsiCo Inc. Revenue growth has halted, but this can be attributed to high revenue growth rates from 2022 to 2024, with the company now reaching a plateau.

The analysis of PEP stock shows that the company’s shares are appropriate for conservative investors who do not chase high returns and prefer moderate but stable growth. For comparison, the S&P 500 index has gained 163% from a low in March 2020 to the present, while PepsiCo stock only rose by 93% over the same period.

PepsiCo Inc. is a dividend aristocrat that consistently increases payouts to its shareholders, offering another reason to favour long-term investments. From 2000 to 2024, the dividend amount increased by 870% and currently stands at 1.36 USD per share.

As previously mentioned, a prolonged period of deflation could pose a significant risk for the company. In such a case, consumers may be inclined to save money, and PepsiCo would need to adapt to the new conditions again. However, after overcoming this period, the company will undoubtedly be able to achieve an even stronger position than before.

การคาดการณ์ที่นำเสนอในส่วนนี้จะสะท้อนให้เห็นความคิดเห็นส่วนตัวของผู้แต่งเท่านั้น และจะไม่สามารถถูกพิจารณาว่าเป็นแนวทางสำหรับการซื้อขาย RoboForex ไม่รับผิดชอบสำหรับผลลัพธ์การซื้อขายที่อ้างอิงตามคำแนะนำการซื้อขายที่อธิบายเอาไว้ในบทวิจารณ์การวิเคราะห์เหล่านี้